Fibre, infrastructure competition, a USO but no Duct Co

Ofcom today published their initial conclusions from the Digital Communications Review that they kicked off last year. Whilst these are officially their interim findings, the direction of travel is relatively clear; over the next 10 years, the UK will move towards an increasingly all-fibre future, with widespread availability of competing fibre networks driving the take-up of ultrafast services underpinned by a USO. Against the background of convergence, Ofcom will do more to make it easier to compare quality of service across fixed, mobile and bundled offers. Openreach understandably lies at the heart of much of this and whilst BT will be sure to feel additional pain, Ofcom are not proposing full structural separation, yet.

Fibre

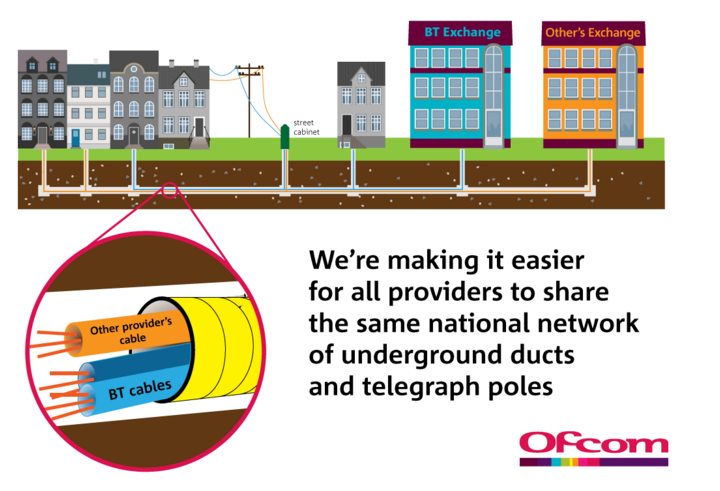

Ofcom have come firmly down on the need for infrastructure competition to provide the necessary investment in fibre networks to enable the UK to build on its current position as a global leader. They have neatly coupled this with a desire to both boost the Quality of Service that Openreach delivers to its users, and reduce the “country’s reliance on Openreach???. Ofcom sets a ‘good outcome’ of network competition at around 40% of households. This focus moves the dial away from the service level focus that has prevailed for the last decade.

To incentivise and encourage this investment, Ofcom have made clear that they will be prepared to deregulate in areas which are seeing high levels of competition and will set prices for ultrafast products that incentivise operators who are building new networks. The major step though, is that Ofcom have committed to making it easier for providers to access Openreach’s ducts and poles. Whilst BT already offers Passive Infrastructure Access (PIA), Ofcom are proposing changes to the information provided, the principle of equivalence of inputs to apply and making access available for businesses as well as households.

Universal coverage

This ultrafast future will be underpinned by a Universal Service Obligation (USO). The UK Government are due to consult on this shortly but Ofcom come firmly down on a USO of 10 Mbit/s download as a safety net for those households (currently 2.4m or 8%) who cannot access this ‘decent’ level. Importantly, Ofcom also referred to the need to include a ‘mechanism for increasing the level of performance delivered over time’ as consumers’ expectations and data consumption continue to rise.

How to frame any target on universal coverage and how to implement it are questions which the BSG will be exploring on the 14th of March at an event bringing together the fixed and mobile industry as well as Government and other experts.

Ofcom also set out the need to boost the deployment of mobile services and superfast connections.

This would mean facilitating the deployment of new technologies (such as long-reach in the hardest-to-reach areas), setting new coverage obligations on network operators winning 700Mhz spectrum licence fees and providing consumers with information on mobile coverage in their local areas.

For mobile operators, Ofcom also said that they would assist the Government in reforming the Electronic Communications Code (expected in the forthcoming Digital Economy Bill) in an effort to make deploying new infrastructure easier. It also committed to examining the deployment of newer technologies such as mobile repeaters or white space devices.

BT and Openreach

Of course, even with increasing competition from Virgin Media as well as alternative providers, and if the new PIA model is a success, many consumers will still rely on services and competition within the Openreach network. That is why Openreach’s independence and governance within the wider BT group has been subject to much of the focus of the review.

Ofcom have stated quite starkly that the status quo is not acceptable but has, crucially, stopped short of recommending that the Competition and Markets Authority investigates whether Openreach should be structurally separate. For the moment at least. Rather, it has sketched out a preferred option of strengthening functional separation, perhaps by making Openreach a wholly owned subsidiary of BT Group with a separate board.

This wouldn’t be an instant panacea as there would need to be clear processes for involving all of Openreach’s customers in its strategic decision making. Ofcom have said that they will be discussing the options available to it with the European Commission and will bring forth detailed proposals later this year. They also say that they are ‘open to voluntary proposals’ which surely means that BT have a chance to negotiate with wider industry to come up with a solution that is palatable to them. This would help resolve the uncertainty and lower the chances of lengthy legal battles.

Convergence

The whole review is taking place with the understanding that we will increasingly see the effect of convergence on the market. This is reflected in Ofcom outlining certain areas, such as voice, which it may deregulate, as well as ensuring that consumers are bundled as services are bundled together. This is why they are bringing forward more information on the quality of service of each part of the bundle and making sure that switching rates do not drop below appropriate levels that you would expect in a competitive market.

This story of course has a long way to go, with much of the detail to be unveiled over the next 12 months in market specific reviews, but at the moment it looks as though Ofcom have balanced investment incentives with concerns over consumer protection.