Ofcom passes the USO back to Government

Ofcom today published their technical advice to Government on the design of a broadband Universal Service Obligation. Ofcom were instructed to deliver its “views, evidence-based analysis and…recommendations??? by John Whittingdale, then Secretary of State for DCMS, in March 2016. It has certainly delivered on the first two although in making clear that designing a USO is complex, it only offers a few recommendations. It will now be up to Government to make some of the thornier policy choices.

Matthew Evans, CEO of the BSG said “Ofcom have produced a comprehensive report that clearly outlines the benefits and challenges of delivering a broadband USO. It is now up to Government to work with industry to ensure that this intervention delivers an appropriate safety net which increases the number of premises that access a good quality broadband connection.”

Defining ‘decent’ broadband

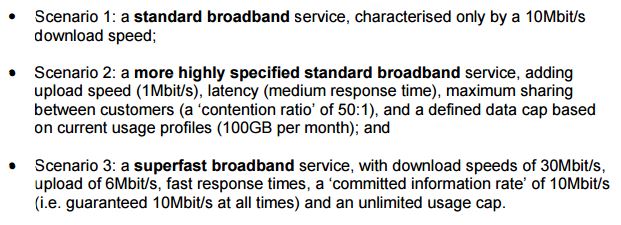

One of the biggest issues is of course defining what the USO should deliver. This has one of the largest impacts on following decisions about costs, benefits and indeed a future review. Ofcom have chosen to model three scenarios. Two that more closely mirror the concept of a USO that is a ‘safety net’ and a third that constitutes a wider public policy target:

It will be interesting to see Government’s response to these scenarios. The third is what the current BDUK intervention delivers and would raise questions about the Government’s rationale for pursuing a different approach to the remaining 3-4% that would not be addressed by either commercial or BDUK deployments.

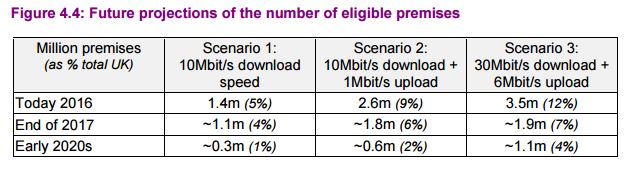

Scale of the problem

Naturally this depends on both the timeline and the scenario considered. Analysys Mason have conducted a study into the project scale of the problem. Government have stated that a USO should apply before the end of the Parliament and the length of time required to design any solution would likely mean that 2020 is a reasonable timeframe:

Who can access and how?

Ofcom dedicate a portion of their evidence to both who should be able to access it – the difference between ‘everyone’ and those in areas that currently do not have ‘decent’ broadband is clearly important. They come down on the former but also make clear that thought must be given the user journey on how they discover whether they are eligible or not. Awareness of the USO is an issue that Ofcom commits to monitoring over the course of the intervention.

A thornier issue is pricing. Here Ofcom merely present the different views that responded to its call for inputs and highlights some consumer research that it carried out on whether there should be a nation-wide price or differences between regions.

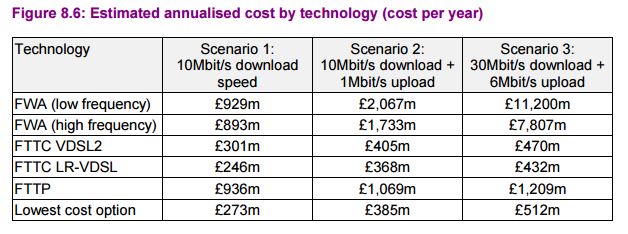

What can deliver ‘decent’ broadband and cost

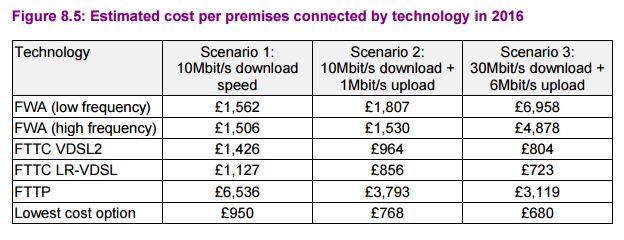

Here is where the definition of decent broadband has a significant impact. Clearly some technologies have more attractive attributes when it comes to upfront vs ongoing costs vs capability of delivering high bandwidth unlimited connections. For that reason satellite is excluded from scenario 2 and 3.

Whilst all such estimates need to taken with a pinch of salt, Ofcom then outline some of the potential costs for the scenarios as well as the up-front and ongoing costs of different technology solutions. The below costs are 2016 figures:

In doing so it highlights the need for a reasonable cost threshold in order to maintain value for money – illustrating that some premises would cost around £45,000 to provide a connection to them. This is clearly an important issue and one which the BSG is currently seeking to address.

Funding

Another big question. The Government has stated that its preference would be for an industry levy of some sort. Ofcom leaves this open but some difficulties in the design of such a scheme. Ofcom seems to move towards a fund made up of fixed and mobile players as one that best balances the benefits and distortions but are clear that this would need further work. An industry levy would also clearly have some impact on consumer prices. Whilst the costs of this depend on a very complicated range of policy levers Ofcom believe that at scenario 3 it could £1.60/month to fixed subscribers.

Who gets to be Universal Service Provider?

Ofcom is clear that there are few providers who could bear the upfront cost associated with being the USP and that a region based solution which would lessen the cost risks causing fragmentation and not delivering value for money. It therefore points strongly towards BT and KCOM although leaves the door open for some local USPs to emerge.

Review

Ofcom identify this as one of the hardest to address as it is linked to the design of the service (broadly scenario 2 and 3 should meet users’ needs for longer) and also affects cost recovery. Ofcom calls on Government to at least indicate the date of the first review to provide industry with some assurances.